Table of Content

- Publication 936 ( , Home Mortgage Interest Deduction

- Can I claim tax benefits if I borrow money from family members or friends?

- Deduction under Section 24 is also available to buyers who do not use home loan

- Tax Breaks for Second-Home Owners

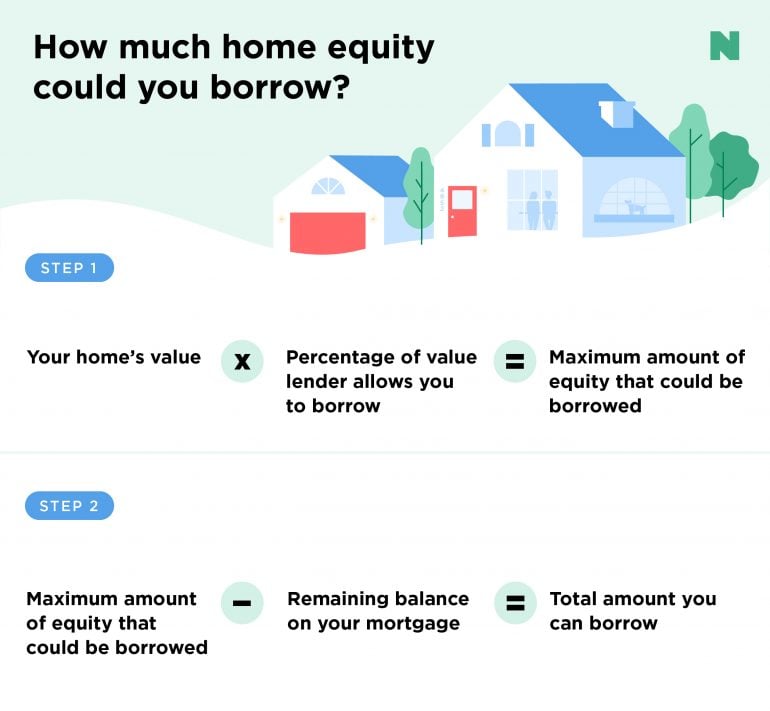

- Is Home Equity Loan Interest Tax Deductible?

- Other Loans & Products

- How much tax benefit can I claim on home loan interest for rented property?

See the earlier discussion of Points to determine whether you can deduct points not shown on Form 1098. Bill used the funds from the new mortgage to repay his existing mortgage. Although the new mortgage loan was for Bill's continued ownership of his main home, it wasn't for the purchase or substantial improvement of that home. He can deduct two points ($2,000) ratably over the life of the loan. He deducts $67 [($2,000 ÷ 180 months) × 6 payments] of the points in 2022. The other point ($1,000) was a fee for services and isn't deductible.

However, the amount of home loan available to you for all the properties taken together, shall depend on various factors like your earnings, age and your ability to service the loan. You are entitled to certain tax benefits, with respect to the interest paid on money borrowed, for buying, constructing, renovating or repairing a house property. The tax laws also allow you claim tax benefits with respect to repayment of the principal amount for buying and constructing a residential house. This deduction too can be claimed, only after you have taken possession of the property. If you have started repaying the principal of a home loan before taking possession, you cannot claim any tax benefits for such payment, either now or in future.

Publication 936 ( , Home Mortgage Interest Deduction

Don't include points or mortgage insurance premiums on this line. In 2022, Bill refinanced that mortgage with a 15-year $100,000 mortgage loan. To get the new loan, he had to pay three points ($3,000). Two points ($2,000) were for prepaid interest, and one point ($1,000) was charged for services, in place of amounts that are ordinarily stated separately on the settlement statement.

For maintenance purposes and general upkeeps, the owner of that ‘let-out property’ can claim a tax rebate of 30%. While a housing loan can help you get a house for yourself; it can also turn out to be an expensive affair. But the various tax benefits that come with such a loan help you save money every year. Take a look at how you can make the most of these benefits.

Can I claim tax benefits if I borrow money from family members or friends?

However, if the property later becomes a qualified home, the debt may qualify after that time. If you receive a Form 1098 from the cooperative housing corporation, the form should show only the amount you can deduct. At least 90% of the corporation's expenditures paid or incurred during the year are for the acquisition, construction, management, maintenance, or care of corporate property for the benefit of the tenant-stockholders. Deduct home mortgage interest that wasn't reported to you on Form 1098 on Schedule A , line 8b.

By communicating with us by phone, you consent to calls being recorded and monitored. If you’re thinking of buying a second home, you’ll probably discover there aren’t quite as many tax advantages with a second home compared to an investment property. This makes sense though, as the purpose of an investment property is the financial opportunity. Whereas, a second home is often used for personal enjoyment. The IRS limits you to one qualified second home for mortgage interest deduction, even if you haven’t met the limit of $750,000/$375,000. The Internal Revenue Service has set guidelines for when a home is considered a second home instead of a rental property.

Deduction under Section 24 is also available to buyers who do not use home loan

This can be claimed in five equal instalments from the year in which construction is completed. This deduction is available with other eligible items like provident fund contribution details of which you can check on UAN member portal, life insurance premium, tuition fees, PPF contribution , NSC, ELSS, etc. This deduction is also available for any amount paid for registration and stamp duty of a residential house. The income tax laws do not have any restriction on the number of houses for which you can claim this deduction. The income tax laws also do not distinguish between self-occupied property or a let out property, for this purpose. So, although, you can take home loans for more than one property, the aggregate amount of deduction shall be restricted to Rs 1.5 lakhs, for repayment of the principal amount of all the home loans taken together.

With rentals, the number of days you rent the property—as opposed to living in it yourself—also comes into play. If the second home is considered a personal residence, you must file Form 1040 or 1040-SR and itemize deductions on Schedule A to claim the mortgage interest deduction. Additionally, the mortgage must be a secured debt on a qualified home in which you have an ownership interest. Tax deduction on the principal component is limited to Rs 1.50 lakhs per annum under Section 80C, while rebate towards interest is capped at Rs 2 lakhs.

You treat your payments as level even if they were adjusted from time to time because of changes in the interest rate. The total of the mortgage balances for the entire year is within the limits discussed earlier under Home Acquisition Debt. A mortgage that doesn't qualify as home acquisition debt because it doesn't meet all the requirements may qualify at a later time. For example, a debt that you use to buy your home may not qualify as home acquisition debt because it isn't secured by the home. However, if the debt is later secured by the home, it may qualify as home acquisition debt after that time. Similarly, a debt that you use to buy property may not qualify because the property isn't a qualified home.

According to Amit Modi, director of ABA Corp and president-elect, CREDAI Western UP, the deduction of principal amount on housing loan should not be clubbed with other deductions under Section 80C. “The deduction should be allowed separately, over and above the limit of Rs 1.50 lakhs under Section 80C. The limit under Section 80C should also be increased to Rs 3 lakhs in the Budget 2021,” Modi said. In fact, industry body CREDAI has suggested that in Budget 2021, the deduction limit under Section 80C for principal repayment on home loans be increased, to make the provision more exhaustive.

The other property, being self-occupied, will have NIL income, but interest deduction on the corresponding home loan, if any, is limited to Rs.2 lakh. Owing to a significant reduction in interest rates, most individuals are leaning towards home loans to finance a property purchase. If you are making such investments for the second time and acquiring funds for that through a home loan, there are certain tax rebates you can enjoy. As per the current provisions, tax benefits are applicable on payable interest.

The IRS is committed to serving our multilingual customers by offering OPI services. The OPI Service is a federally funded program and is available at Taxpayer Assistance Centers , other IRS offices, and every VITA/TCE return site. The OPI Service is accessible in more than 350 languages. You paid for the home with cash you got from the sale of your old home.

Owing to the difficulties caused by the Coronavirus pandemic, there was a demand from sector stakeholders, to extend this time limit further, in order to incentivise buyers. Consequently, finance minister Nirmala Sitharaman extended the scope of this section for another year, i.e., till March 31, 2022, to provide an impetus to the sector. This is why there has been a long-standing demand that the deduction limit under Section 80C be increased, in order to justify the vast number of investment/expenditures it covers.

The mortgage interest deduction is a popular tax break that allows homeowners to write off the home loan interest they pay each year. Eligibility period for claim of additional deduction for interest of Rs.1.5 lakh paid for loan taken for purchase of an affordable house extended till 31 March 2022. The following table gives you the tax benefits under the corresponding sections of the Income Tax Act, 1961. Union Finance Minister Nirmala Sitharaman in the budget speech proposed to extend the deadline for availing additional deductions on interest payment on home loans to 31 March 2024. This comes after the government had in the previous budget extended the deadline to 31 March 2022. The extension on home loans till 31 March 2024 is applicable for all home loans sanctioned till 31 March 2022.

You will include the interest for January 2023 with other interest you pay for 2023. In the year paid, you can deduct $1,750 ($750 of the amount you were charged plus the $1,000 paid by the seller). You must reduce the basis of your home by the $1,000 paid by the seller.

No comments:

Post a Comment